Cat bond market participants held their collective breath last week as hurricane Matthew approached the eastern seaboard of the United States. This tropical storm formed near St. Lucia in the Antilles on 28 September and initially moved west over the Caribbean Sea, intensifying to a hurricane on 29 September, before turning north and crossing the western tip of Haiti, causing significant amounts of damage to property and loss of life.

Cat bond market participants held their collective breath last week as hurricane Matthew approached the eastern seaboard of the United States. This tropical storm formed near St. Lucia in the Antilles on 28 September and initially moved west over the Caribbean Sea, intensifying to a hurricane on 29 September, before turning north and crossing the western tip of Haiti, causing significant amounts of damage to property and loss of life.

Cat bond market participants held their collective breath last week as hurricane Matthew approached the eastern seaboard of the United States. This tropical storm formed near St. Lucia in the Antilles on 28 September and initially moved west over the Caribbean Sea, intensifying to a hurricane on 29 September, before turning north and crossing the western tip of Haiti, causing significant amounts of damage to property and loss of life.

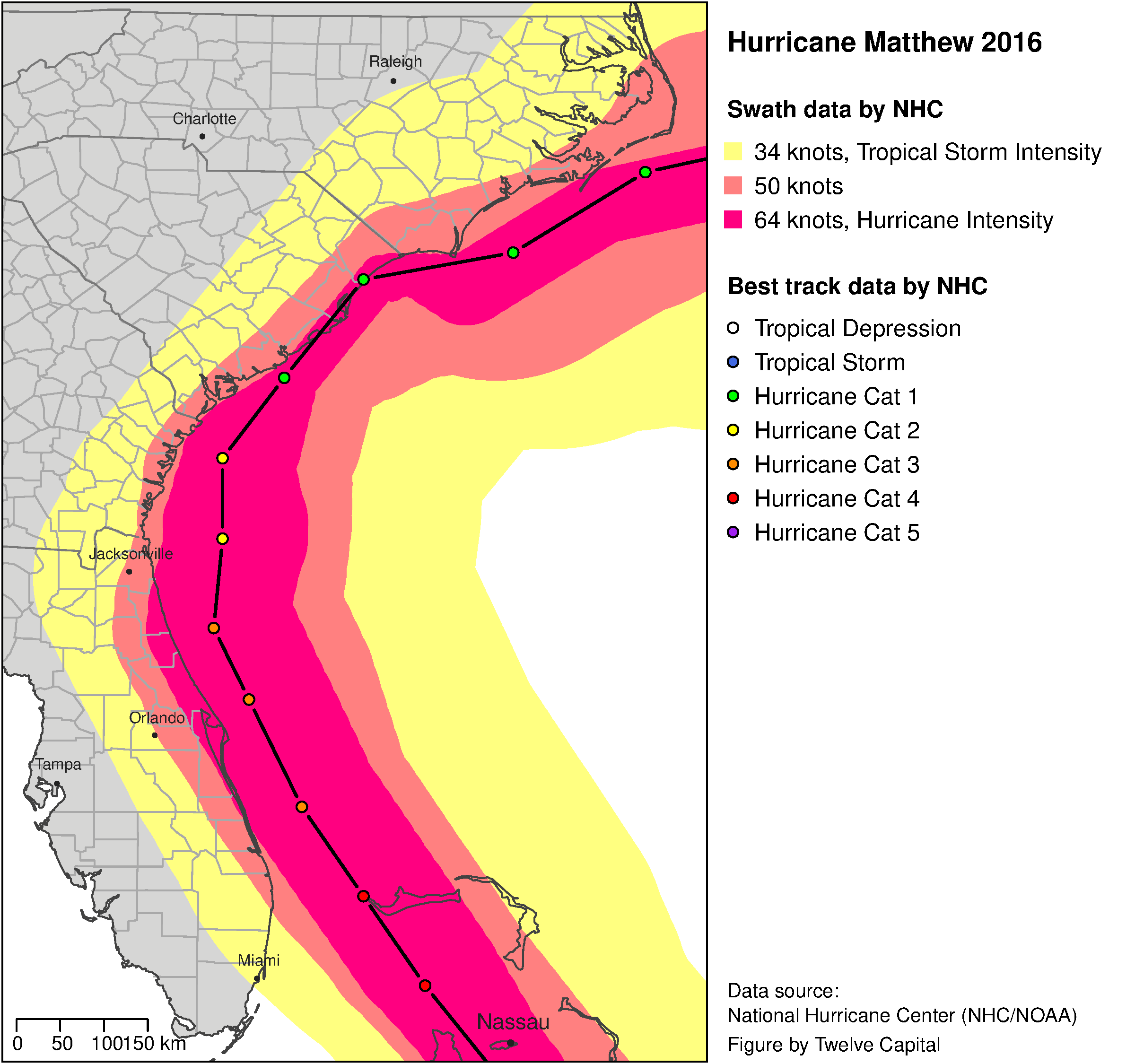

For reinsurers and ILS fund managers, to know what the risk is from hurricanes such as Matthew, a variety of quantitative methods are employed that can be used to ‘predict the unpredictable’ or, rather, ascribe a greater degree of accuracy to assessing the likelihood of default for a catastrophe bond in comparison to many corporate bonds in the market.Although Matthew intensified to a category 4 hurricane over the Bahamas, it was downgraded to a category 3 storm before approaching and moving along the Floridian coast. As Matthew headed north, it weakened to a category 2 storm whilst progresing along the Georgia coast and was finally downgraded to category 1 while moving along the coast of South and then North Carolina.According to a preliminary wind field published by the National Hurricane Center of the US National Weather Service, only a small area over land was affected by hurricane force winds in the United States (see chart inset – click to enlarge).The overall impact on losses is therefore expected to be limited, with the latest updates from catastrophe risk modelling agencies indicating that cat bonds are unlikely to have been affected by the hurricane, although it will take a few weeks until final loss estimates are available. Hurricane Matthew and the cat bond market Although having caused devastation and many hundreds of deaths in Haiti, hurricane Matthew caused less damage in the Bahamas and Florida and, as a result, investors in the alternative asset class of catastrophe bonds could, pending final loss estimates, find that their investments are not at risk at this time.Indeed, cat bonds provide a degree of protection to (re)insurance companies against claims that are the result of large natural catastrophes such as hurricanes. Since these modern reinsurance vehicles are often positioned in senior layers of a company’s reinsurance programme, it generally takes a “substantial” event to trigger any pay-out or, indeed, a default of the bond.In this context “substantial” typically refers to hurricanes with class 2 wind forces or more, however pure parametrically triggered cat bonds, which have pay-out mechanics subject to measured windspeeds only, are rare. The more common type of cat bond triggers are indemnities, where the erosion of principal depends on actual losses sustained by the sponsor of the cat bond.Experience shows that losses to property from wind forces have shorter development patterns than earthquake losses for instance and, given that Matthew is expected to have caused total damage to the insurance industry of approximately USD 3bn to 9bn (according to the latest figures published by AIR), a low number in a relative context, this shortens the development period even further and reduces the likelihood of a cat bond being triggered.Predicting the unpredictable Catastrophe models are based on a mixture of historical data, geophysical knowledge and statistical models, which have been used by the reinsurance indstury for the last 30 or so years. Historical data for Atlantic hurricanes, for instance, is available for more than 150 years, with at least 50-100 years of this considered to be complete and reliable. Such data can then be used to form the underlying foundation of a statistical model which, using the geophysical knowledge available on hurricane formation, can produce thousands of years of hypothetical storms to analyse. Although these are only hypothetical storms, they could occur given that such events follow the same overall statistics and rules as storms experienced in the past.After this, a wind field is calculated around each of those storm tracks which has a maximum wind speed ascribed to them at each building location within the insurance portfolio. As a result, the insured loss to an insurance portfolio for all of the thousands of years of hypothetical storms can be quantitatively calculated, whilst avoiding many of the qualitative assumptions that those analysing traditional corporate bonds may also have to incorporate into their analysis.Many catastrophe bond strategies aim to use the above analysis to deliver positive risk-adjusted returns by quantitatively analysing and investing in a portfolio of public and, sometimes, private cat bonds, covering the risk of defined insurance events (usually natural catastrophe perils). They have a number of attractive investment features including mid-single digit historical returns, low historical average volatility, low correlation to mainstream financial markets, diversification properties, minimal counterparty risk and minimal duration risk.Sandro Kriesch (pictured) is head of ILS and Jan Kleinn is head of ILS analytics at Twelve Capital.

Sign up to the portfolio institutional newsletter to receive a weekly update with our latest features, interviews, ESG content, opinion, roundtables and event invites. Institutional investors also qualify for a free-of-charge magazine subscription.